Coronavirus Job Retention Scheme

The Coronavirus Job Retention Scheme has been extended until 30 September 2021 and the level of grant available to employers under the scheme will stay the same until 30 June 2021.

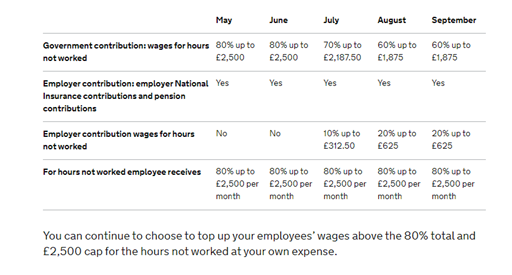

The current version of the furlough scheme that started on 1 November 2020 was scheduled to end on 30 April 2020. In order to avoid a “cliff-edge” with resulting widespread redundancies the chancellor has announced a further extension of the scheme and also a phased reduction in support to employers. The CJRS furlough grant for May and June will remain at 80% of the employees’ usual pay for hours not working.

From 1 July 2021, the level of grant will be reduced, and you will be asked to contribute towards the cost of your furloughed employees’ wages. To be eligible for the grant you must continue to pay your furloughed employees 80% of their wages, up to a cap of £2,500 per month for the time they spend on furlough.

The scheme will then be limited to 70% for July and then 60% for August and September. This phased reduction will operate in a similar way as in September and October 2020 with the employer being required to contribute the remaining 10% and then 20% of an employee’s regular pay so that they continue to receive 80% pay for furloughed hours.

In addition to the 10% and 20% contributions employers will continue to be responsible for paying employers national insurance and pension contributions on the full amount being paid to employees.

The table below shows the level of government contribution available in the coming months, the required employer contribution and the amount that the employee receives per month where the employee is furloughed 100% of the time.

Wage caps are proportional to the hours not worked.

Please contact us if you want an estimate of the claim or you need help in applying.